RBI and SEBI Compliance for FinTechs: What Your Security Team Needs to Know in 2026

-

Shankar Jayaraman

Shankar Jayaraman - 19 May, 2026

Navigating RBI and SEBI compliance in 2026 is critical for FinTechs in India. With intensified regulations and overlapping requirements, security teams must stay ahead to avoid penalties and ensure smooth operations.

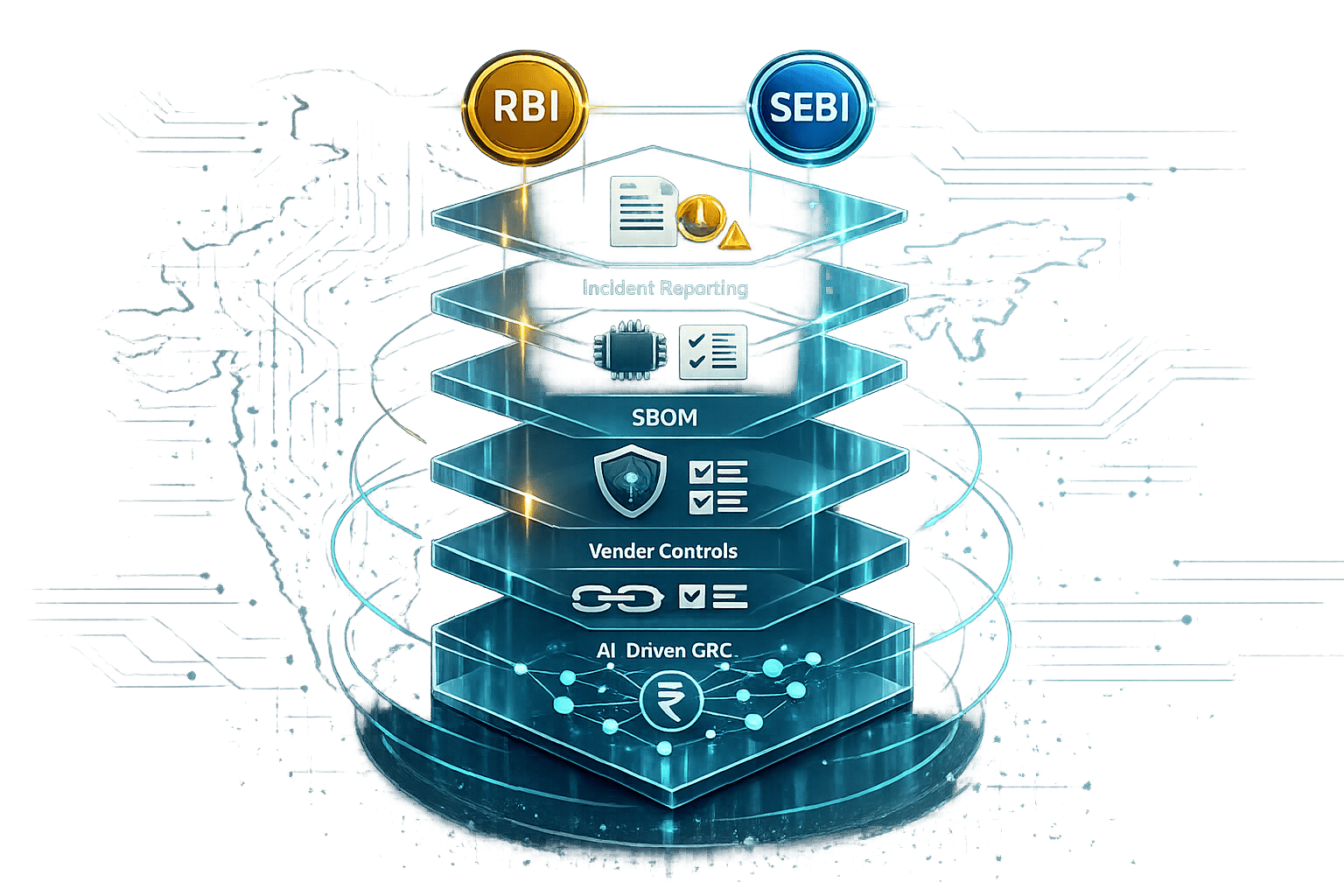

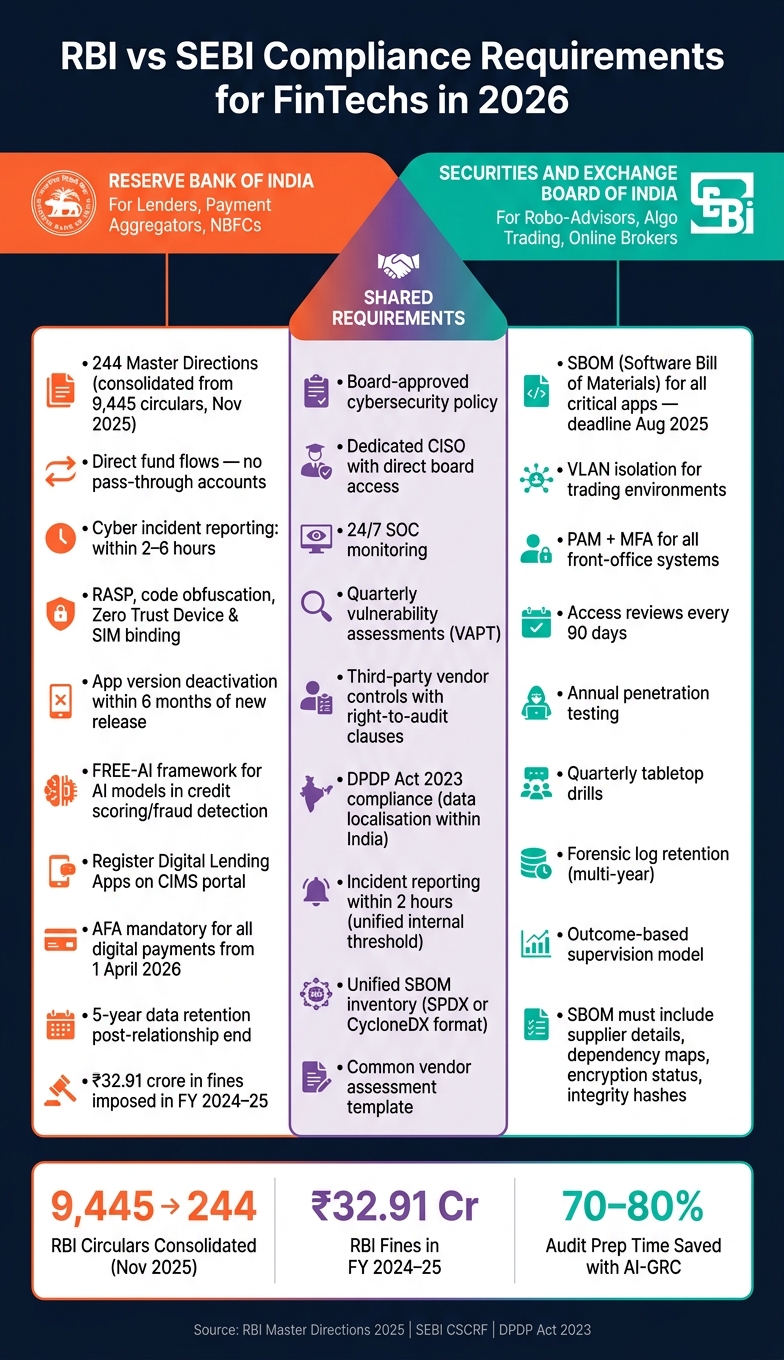

- RBI tightened rules: 244 unified Master Directions replaced 9,445 circulars in November 2025. Key mandates include direct fund flows, cyber incident reporting within 2-6 hours, and stricter app security controls.

- SEBI’s focus on resilience: SEBI expects SBOM, VLAN isolation, and regular cyber resilience checks for market-linked FinTechs.

- Overlapping demands: Both regulators require board-approved cybersecurity policies, 24/7 SOC monitoring, and strict third-party vendor governance.

- Penalties are high: RBI imposed ₹32.91 crore in fines in FY 2024-25, with NBFCs heavily impacted.

Actionable Steps

- Build a unified compliance control map across RBI and SEBI obligations.

- Use autonomous AI agents for evidence collection and reporting.

- Prioritise controls for payment rails, lending systems, and customer-data pipelines.

Compliance is not just about avoiding penalties - it is a trust and growth accelerator.

Breaking Down RBI and SEBI Compliance Requirements

RBI vs SEBI Compliance Requirements for FinTechs in 2026

RBI Compliance Areas Security Teams Must Address

RBI’s consolidated Master Directions simplified the rulebook but raised expectations for implementation rigor.

Key areas include:

- Digital lending controls: direct borrower-to-lender fund flows, no pass-through pools.

- Cyber incident reporting: accelerated reporting windows.

- Mobile and app security: RASP, code obfuscation, and strict app lifecycle controls.

- AI model governance: explainability and risk review for model-driven financial decisions.

SEBI Cyber Resilience Requirements for Market-Linked FinTechs

For brokers, robo-advisors, and trading-linked platforms, SEBI places heavy emphasis on operational cyber resilience.

Key expectations include:

- SBOM for critical applications and dependencies.

- Network segmentation and privileged-access controls.

- MFA and access reviews for sensitive systems.

- Regular testing (including drills, pentests, and resilience exercises).

Where RBI and SEBI Requirements Overlap

| Compliance Area | RBI Requirement | SEBI Requirement | Unified Approach |

|---|---|---|---|

| Governance | Board-approved cyber policy; CISO responsibility | Board-approved cyber resilience policy | Single board-approved policy and one accountable CISO |

| Monitoring | Continuous SOC visibility | 24/7 SOC and segmentation expectations | Unified 24/7 SOC with shared telemetry |

| Incident Reporting | 2-6 hour reporting windows | Fast severe-incident escalation | Internal 2-hour triage/escalation SLA |

| Software Risk | CERT-In aligned software risk controls | SBOM for core apps | Unified SBOM inventory in standard formats |

| Vendor Risk | Right-to-audit and localisation obligations | Strong due diligence and security SLAs | Common vendor governance and assessment template |

How to Operationalise RBI and SEBI Security Requirements

Governance and Oversight

Boards must receive regular cyber risk updates, and CISO accountability should be explicit. A single cross-regulator governance model improves clarity and reduces duplicated effort.

Technical Controls

Core controls should include:

- 24/7 SOC monitoring,

- periodic VAPT,

- strong API security (OAuth2, tokenisation, rate limits),

- strict patching SLAs,

- and log retention aligned to regulatory expectations.

Third-Party Risk Management

Contracts should include right-to-audit clauses, localisation obligations, incident SLAs, and measurable remediation timelines. Tier vendors by risk and apply depth of review accordingly.

Building a Unified Multi-Framework Compliance Architecture

Map Once, Reuse Across Frameworks

Controls like MFA, encryption, privileged access, and VAPT can be mapped once and re-used across RBI, SEBI, DPDP, ISO 27001, and SOC 2 evidence models.

Common Pain Points

FinTechs often struggle with:

- overlapping circulars and directives,

- repeated evidence requests for similar controls,

- fragmented toolchains,

- and compressed reporting deadlines.

Design a Risk-Led Control Framework

Start with the highest-risk systems and data pathways, then align controls to all applicable frameworks. This avoids checklist fatigue and improves real risk reduction.

Using AI-Native GRC Platforms for Continuous Compliance

Core Capabilities

AI-native GRC platforms reduce manual effort by:

- collecting evidence continuously from cloud, identity, and DevOps systems,

- mapping controls to multiple frameworks,

- surfacing control drift in real time,

- and generating audit packs on demand.

How CISOGenie Helps

CISOGenie supports 35+ frameworks and enables a “map once, reuse everywhere” model for ongoing compliance operations. This is especially useful for overlapping RBI-SEBI obligations and rapid incident response requirements.

Practical Rollout Sequence

- Obligation mapping: map product features to regulator obligations.

- Governance setup: define ownership, escalation, and board reporting.

- Control integration: connect agents to cloud/identity/dev tooling.

- Real-time cockpit: monitor control health and risk continuously.

- Audit automation: generate evidence bundles and keep control maps current.

Conclusion: Turn Compliance into a Long-Term Advantage

RBI and SEBI compliance in 2026 should be treated as an operating capability, not a legal afterthought. FinTechs that embed compliance into architecture, product design, and vendor governance gain speed, trust, and resilience.

AI-enabled, risk-led GRC turns audit cycles from periodic panic into continuous readiness - while reducing duplicated effort across frameworks.

FAQs

Which RBI and SEBI rules apply to my FinTech?

It depends on your business model (lending, payments, broking, advisory). Most firms face overlapping obligations in governance, incident response, customer protection, and third-party risk. Build a product-to-regulation mapping early.

How can we meet the 2-6 hour incident reporting deadline?

Use automated detection, predefined severity triage, and rapid escalation workflows. Manual-only processes are usually too slow for regulator timelines.

How can we avoid duplicate audits across RBI, SEBI, DPDP, ISO 27001, and SOC 2?

Adopt a unified control model with continuous evidence capture. Map shared controls once and re-use evidence across frameworks through an AI-native GRC platform.